Validate your benefits package with our new benchmarking tool.

Learn about My Future Fund, Ireland's Auto Enrolment pension scheme launching in 2025. Discover eligibility, contributions, and how it works.

.webp)

.webp)

.png)

.png)

.png)

Ireland has named its proposed Auto Enrolment pension scheme "My Future Fund".

Is it just a name change, or are there important updates employers need to know?

Let’s find out what this means for your business.

My Future Fund is Ireland's new Auto Enrolment retirement savings scheme, set to launch on 30th of September, 2025.

It aims to improve pension coverage for 750,000 private sector workers in Ireland who currently lack retirement savings beyond the State Pension, strengthening Ireland's overall pension system.

The scheme will automatically enrol eligible employees in a pension plan, with contributions from the employee, employer, and the Irish government.

According to Heather Humphreys, the Minister for Social Protection, the new name, "My Future Fund," is meant to make people feel more connected to their pension. It encourages them to take a more active role in saving for retirement.

It’s just a rebranding of the scheme that was previously known as “Auto Enrolment”.

The rules about who can join and how the scheme works are unchanged.

Let’s quickly go over that next.

To be automatically enrolled in My Future Fund, an Irish employee must:

Part-time and seasonal workers who meet the age and income requirements will also be enrolled.

Exemptions:

An employee will not be auto enrolled if they are already a member of:

To qualify for this exemption, their contributions must be processed through payroll.

The National Automatic Enrolment Retirement Savings Authority (NAERSA) is the administrative body that will oversee My Future Fund in Ireland. They will identify employees eligible for Auto Enrolment, so employers won’t need to assess whether their workers meet the required criteria.

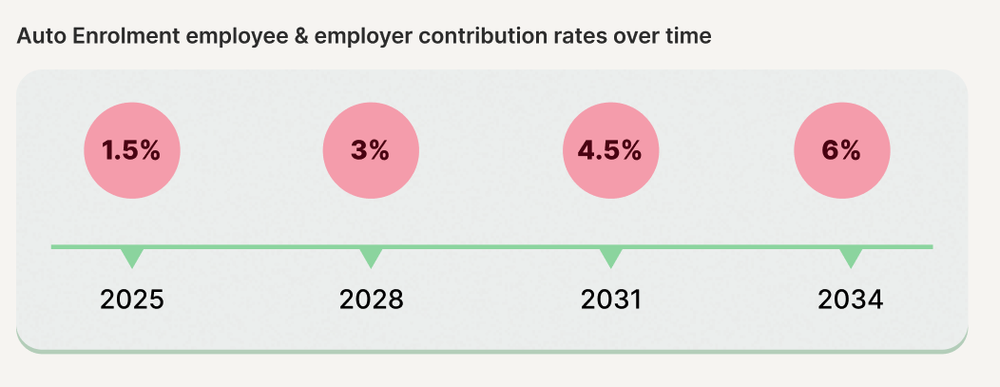

Under My Future Fund, contributions are based on a percentage of an employee’s gross salary, up to a maximum of €80,000 per year.

Contribution rates are introduced gradually through a phasing-in period, which begins with My Future Fund’s launch in 2025 and ends in 2035 when the maximum rate of 6% applies.

Here’s a breakdown of employee, employer, and government contribution rates:

Employee contribution rates will increase gradually in phases:

As an employer, you will be required to match employee contributions. For example, if an employee contributes 1.5%, you will also contribute 1.5%.

The State will support these contributions by adding a top-up amount.

This begins at 0.5% in year 1 and will gradually increase. By year 10, the State top-up will reach 2%.

Auto Enrolment employee & employer contribution rates over time:

For example:

Let's say an employee’s combined income is €40,000 per year. In year 1 of My Future Fund:

This means that in the first year, €1,400 would be added to the employee’s retirement savings.

Unlike My Future Fund, occupational pensions offer greater flexibility.

You can tailor contributions to suit your business and your employees’ financial goals.

Here’s how occupational pension contributions work in Ireland:

Want to set up an Irish occupational pension scheme? Kota can help.

Kota is a digital pensions platform that lets you easily set up a compliant workplace pension in minutes — all without any administrative burden or complex paperwork.

We partner with Irish Life to offer their EMPOWER Personal Lifestyle Strategy (Empower PLS) solution in Ireland, which has two key benefits:

So why wait?

Join Kota to empower your team with flexible, competitive pensions.

Here are some common questions on Ireland’s new Auto Enrolment scheme:

Employees can’t opt out for the first six months. After that, they have a two-month window (months 7-8) to do so.

If they opt out, they'll automatically be re-enrolled 2 years later.

Employers can't opt out of the scheme. It's a legal requirement, with fines and potential prosecution for non-compliance.

NAERSA will oversee investment management, with major Irish pension providers likely managing the funds.

Most people will start in a default fund that invests in higher-risk options when they're younger, then gradually shift to safer investments as they near retirement. Employees can choose their own funds too.

Stakeholders can refer to our comprehensive Auto Enrolment guide.

You can also contact the Department of Social Protection at autoenrolment@welfare.ie with any questions about My Future Fund or Auto Enrolment.

Trevor Gardiner QFA, RPA, APA in Insurance. With 23 years of experience in Financial Services, I have a strong passion for Health Insurance and Pensions.

.png)

.png)

.svg)

.svg)

.svg)