Occupational Pension vs Auto Enrolment Ireland: Which Is Right for You?

Learn the key differences between occupational pension and the Auto Enrolment scheme in Ireland. Find the right option for your business.

Article written by

Trevor Gardiner

Enjoying this article?

Share it with the world!

Occupational pension schemes and Auto Enrolment are two distinct approaches to retirement savings in Ireland.

With Auto Enrolment set to launch in January 2026, employers and employees must understand how it compares to traditional occupational pension schemes.

We’ll compare them in detail to help you determine the right option for your needs.

Occupational Pension vs Auto Enrolment in Ireland

Let’s first understand what occupational pensions and Auto Enrolment mean for businesses and employees in Ireland.

Starting in January 2026, Irish employers will be required to automatically enrol employees aged between 23 and 60 who earn over €20,000 annually in the government-led 'My Future Fund' scheme (run by the newly established National Automatic Enrolment Retirement Savings Authority).

What Is an Occupational Pension Scheme?

An occupational pension scheme (aka a company pension scheme) is an employer-established retirement pension plan designed to provide employees with benefits upon retirement.

These schemes are typically flexible, allowing employers to determine their contribution rates and investment options and offering features like Additional Voluntary Contributions (AVCs).

For employers to be exempt from Auto Enrolment, their occupational pension scheme must meet certain basic criteria — such as having employer contributions (even if minimal) and covering eligible employees.

9 Key Differences Between Irish Auto Enrolment & Occupational Pension Schemes

1. Eligibility Criteria

Occupational Pension Scheme: To be exempt from Auto Enrolment, your scheme must be open to all employees over 23 with earnings above €20,000 from the first day of hire.

Auto Enrolment: Employees aged 23 to 60 with earnings above €20,000 annually are automatically eligible and enrolled.

The pension Auto Enrolment system aims to provide coverage to approximately 750,000 private sector workers without access to occupational pensions. That said, in the scheme’s initial phase, self-employed and non-salaried individuals won’t be eligible for Auto Enrolment.

2. Contribution Rates

Occupational Pension Scheme: To be exempt from AE, Irish employers must provide an occupational pension scheme that meets minimum standards, including offering pension contributions greater than zero during the initial years. An occupational pension can consist solely of employer contributions, without requiring employee contributions.

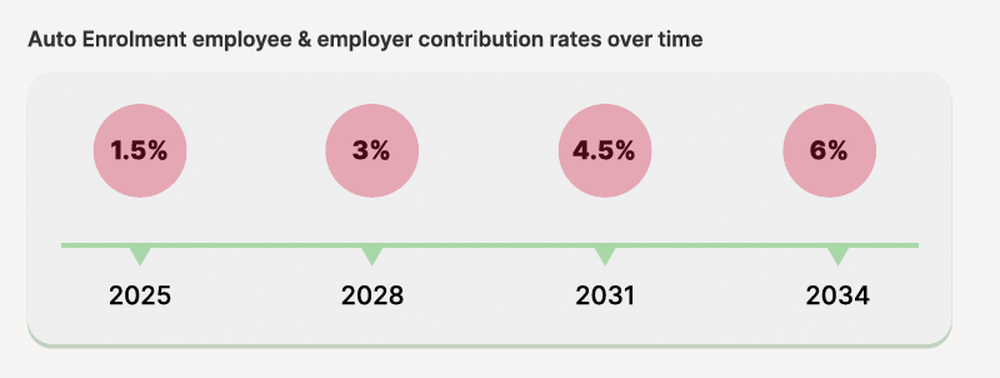

Auto Enrolment: Pension contribution rates start at 1.5% each from employers and employees in the initial phase. This will increase to 6% over time. The Irish government also provides a state contribution, adding a 0.5% to 2% top-up.

3. Earnings Criteria

Occupational Pension Scheme: The scheme must include employees earning €20,000 or more annually to qualify for AE exemption.

Auto Enrolment: Contributions will be calculated based on an employee’s gross earnings.All employees earning over €20,000 annually are included, which aims to target those most in need of a retirement savings scheme.

4. Tax Relief

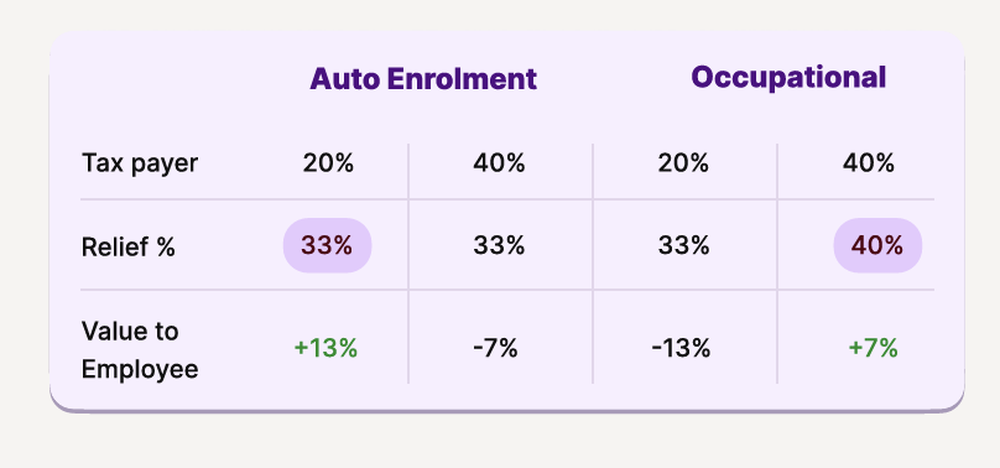

Occupational Pension Scheme: Offers income tax relief on contributions at rates of 20% or 40%, depending on the employee's income level, making it highly tax-efficient.

Auto Enrolment: The State provides a 33% top-up to taxpayers instead of traditional tax relief, simplifying the new system but potentially offering fewer benefits to higher earners.

5. Provisions for Additional Voluntary Contributions (AVCs)

Occupational Pension Scheme: Employees can make AVCs to increase their pension fund, gaining greater control over their savings.

Auto Enrolment: AVCs are unavailable under the Auto Enrolment scheme, limiting employees’ ability to save beyond mandatory contributions.

6. Retirement Age and Claim Options

Occupational Pension Scheme: Payouts are generally available from age 50 if the employee has left their employment.

Auto Enrolment: Payouts align with the State Pension age, currently set at 66, which may rise in the future, limiting flexibility for early retirement.

7. Opt-In/Opt-Out Options

Occupational Pension Scheme: Participation is usually voluntary (opt-in), though employers may have to make enrolment automatic to be exempt from Auto Enrolment. They can do this by adding a minimum default contribution for all employees.

Auto Enrolment: Mandatory enrolment with an opt-out option after six months; re-enrolment is required every two years. Those who opt out receive a full refund of their own contributions.

8. Investment of Funds

Occupational Pension Scheme: Employers and employees can choose their investment funds, often working with pension providers to tailor strategies to individual needs. This allows for more aggressive or conservative approaches based on employee preferences.

Auto Enrolment: Employees are placed in a default investment strategy, which may not be tailored to individual preferences, potentially leading to lower returns for some.

9. Management Charges

Occupational Pension Scheme: Charges are set by pension providers, and Kota’s current management charge is 0.75%, which is competitive within the industry.

Auto Enrolment: Expected to have competitive charges, but exact rates are not yet confirmed. The Government have said that they are aiming for under 0.5 % all-in charges.

Occupational Pension or Auto Enrolment Ireland: Which Is Better?

Like any significant change, automatic enrolment in Ireland comes with its share of pros and challenges.

Pros of the Auto Enrolment Scheme

The new system ensures broad participation in retirement savings, as enrolment is automatic for eligible employees.

Contributions are shared between employers, employees, and the Irish government, providing a base level of retirement income.

Challenges With Auto Enrolment

Administrative Burden: Irishemployers have to manage payroll changes, coordinate with the National Automatic Enrollment Retirement Savings Authority (NAERSA), and ensure compliance. The increased administration may require investment in new payroll systems or additional staffing.

Fixed Contribution Requirements: The mandatory employer contributions increase over time, impacting business cash flow. This may especially affect small businesses that may struggle with rising contribution costs.

Limited Flexibility: No AVCs and restricted investment options mean employees have limited ways to boost their pension savings or adjust investment strategies to match their risk tolerance.

Need more flexibility and control over retirement savings?

Occupational pensions may be the better choice for your business and team.

Why an Occupational Pension May Be a Better Choice For Your Business

Flexibility: Employers can determine contribution levels, tailor investment options, and offer AVCs, giving employers and employees more control over their pension provisions.

Higher Contribution Potential: Many employers choose to contribute more than the minimum contributions required under automatic enrolment, potentially resulting in a larger retirement pension fund.

Enhanced employee benefits: Offering a more comprehensive pension coverage package can help attract and retain talent, making occupational pension schemes a strategic choice for businesses.

Tax Efficiency: Contributions to occupational pension schemes provide tax relief that can benefit higher earners significantly, compared to the standardised 33% government contributions in AE. Additionally, employer contributions are eligible for deduction under corporation tax.

Set Up Your Occupational Pension Scheme in Minutes with Kota

Our platform is designed to simplify the process, offering tailored options for contributions, tax relief, and investments.

With Kota, employers have the flexibility to create pension arrangements that work for their teams.

3 FAQs About Occupational Pension & Auto Enrolment in Ireland

We’ll answer some common questions about these pension options:

1. Will the Auto Enrolment Scheme Replace the State, Occupational and Personal Pensions?

No, the Auto Enrolment scheme is designed to supplement the State Pension and won’t replace the existing pension schemes.

Employers who provide a company pension scheme are exempt from AE requirements.

Additionally, employees contributing to private pension schemes like personal retirement savings accounts (PRSA) through their payroll won’t be auto enrolled into the AE scheme.

2. Can Employees Participate in Both Occupational and Auto Enrolment Pension Schemes?

No, if an employee is part of an occupational pension plan, they’re exempt from automatic enrolment and cannot participate in both for the same employment.

3. Is It Better for Employers to Offer Occupational Pensions or Rely on Auto Enrolment?

Occupational pension arrangements provide more flexibility, higher contributions, and greater income tax advantages, making them a superior option for employers who want to provide competitive retirement benefits.

Making the Right Choice: Occupational Pension vs Auto Enrolment Ireland

Choosing between an Auto Enrolment retirement savings system and an occupational pension scheme is a significant decision for employers.

While the Auto Enrolment system takes a standardised approach to pension savings, occupational pensions go beyond — offering higher contributions, tax advantages, and tailored investment options that boost employee satisfaction and retention.

To make the right choice for your business, consult a financial advisor or explore Kota’s pension solutionsto see how we can help.

Article written by

Trevor Gardiner

Trevor Gardiner QFA, RPA, APA in Insurance. With 23 years of experience in Financial Services, I have a strong passion for Health Insurance and Pensions.

.webp)

.webp)

.png)

.png)

.png)

.png)

.png)

.svg)

.svg)

.svg)

.webp)

.webp)

.webp)

.webp)